A study by Federal Reserve economists Elora Raymond and Jessica Dill found that it’s true that first-time homebuyers prefer to buy in the city. They tend to live closer city centers than existing homeowners who are burying a new home. First-timers buy within an average of 5.8 to 5.9 miles from city centers whereas existing owners prefer 6 to y25 miles.

Where millennials settle could determine whether cities continue to grow, what transportation infrastructure expenditures should be, and whether homebuilders should focus their efforts on multifamily housing in urban locations or traditional single-family homes in the suburbs.

A number of observers have speculated whether the recent surge in millennials living in cities represents a change in preferences or whether it’s simply an artifact of financial constraints—tighter underwriting standards, weak income growth, or larger student debt. Nielsen’s survey of young adults found that millennials prefer the lifestyle afforded by dense urban environments, but the National Association of Homebuilder’s survey of young homebuyers finds that just 10 percent would prefer to live in the city while a whopping 66 percent want to live in the suburbs. Setting preferences aside, others debate whether millennials really are moving to the city. While recent data confirm that young people are moving to the cities at much higher rates than in the 1990s, it’s also true that the raw majority of young people choose the suburbs over the city

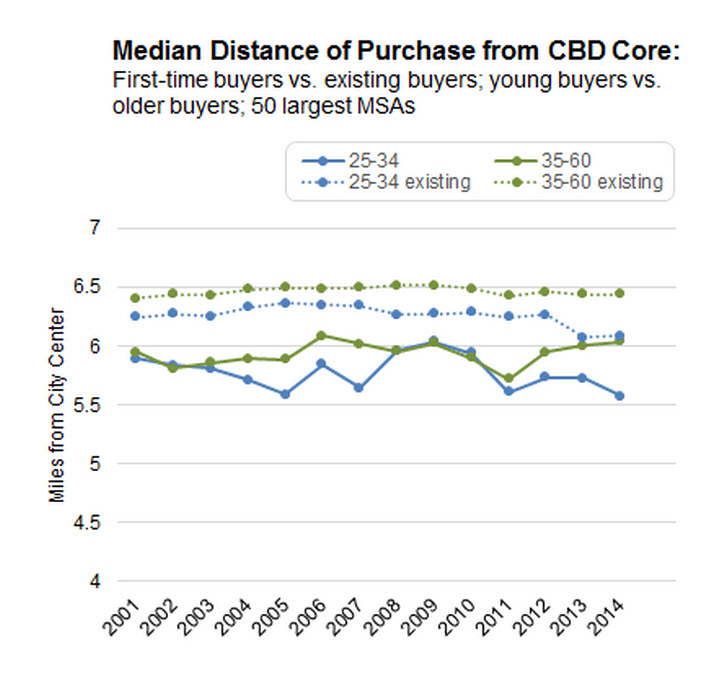

Beginning in 2003, younger first-time homebuyers trended towards more central locations. During the 2007–09 recession, the spread between older and younger first-time homebuyers collapsed. After the recession, the spread widened again. It’s difficult to say whether the shift in purchase patterns is the result of financial constraints or changing preferences, but the tendency appears to be for newer and younger homeowners to purchase homes closer to the city center.

The economists, based in the Atlanta Federal Reserve Bank, assembled a data set that allowed them to identify first-time millennial homebuyers and the census tracts where they bought their first homes.

Using this data, they asked if first-time millennial homebuyers are more likely to live near the city center than either existing homeowners or older first-time homebuyers. Finally, they looked at how other factors like creditworthiness and student debt levels appear to influence this decision.

Below, they charted the median distance from the central business district (CBD) of first-time and existing homeowners by age bracket from the years 2001 to 2014. We find that existing homeowners tend to live, on average, 6.3 to 6.5 miles from the city center.

.What this chart cannot tell us is whether the trend that has younger people living closer to the city center reflects uniform preferences or whether this is an artifact of stronger economic growth in denser cities. In other words, is this trend the result of strong home buying in compact cities and weak sales in sprawling metropolises (that is, between cities), or is it the result of all buyers nationwide choosing to move closer to the city center (that is, within cities)?

To further investigate whether millennials prefer to live close to the city center, the researchers performed several regressions to see how age relates to first-time homebuyer location decisions before and after the crisis. They controlled for credit score, mortgage size, and student debt levels. The sample includes first-time homebuyers aged 18–60 who chose to purchase homes in the 50 largest metropolitan statistical areas (MSA) in the United States. They calculated distance by matching the census tract variable in the Federal Reserve Bank of New York Consumer Credit Panel with census tract data on distance from city center.

Because some cities are more compact than others, we add MSA-level fixed effects. To control for the influence of nationwide effects such as the introduction of quantitative easing and the first-time homebuyer tax credit, we control for year-fixed effects as well in each regression. These controls should adjust for all region and time invariant factors that might affect both the age and location choice of home purchases.

Since creditworthiness typically increases with age and households with higher credit scores tend to be less constrained in their location choice, we also add a risk score variable to see whether age is simply a proxy for the ability to borrow. Similarly, we include mortgage balances. Finally, we add student debt balances to see whether the higher student debt burdens of young people can explain the discrepancy between the location choices of older and younger buyers.

They found that age appeared to have had a small impact on location and was not significant. Other factors such as size of mortgage and amount of student debt seemed to be larger determinants of location. Homebuyers with larger mortgages and with more student debt were more likely to live farther from the city center.

The average distance from city center—five-and-a-half miles—could very well describe areas with moderate density and single-family housing stock in moderate-sized cities. To focus on whether younger homebuyers are interested in living in the central city, they repeated these results using a logistic regression predicting the likelihood a first-time homebuyer will purchase within one mile of the city center. Controlling for all available factors, they found that younger buyers are significantly more likely to live in the heart of downtown. For each additional year, the odds that a buyer will decide to live within one mile of the city center drop by 6 percent.

“Our interpretation of the data suggests that first-time homebuyers became more likely to buy closer to the city center during and after the housing market crisis and that young homeowners (first-time and existing) are more likely to live closer to the city center than older homeowners. Moreover, creditworthiness, total mortgage balance, and student debt loads appear to matter when the time comes to decide where to buy. In short, although age may not affect whether someone buys a house, our analysis suggests it may influence where they buy,” the researchers concluded