Chronically low interest rates may have accomplished something that the housing lobby has spent millions of campaign contributions and decades of political pressure to prevent.

Did the mortgage interest deduction, long the holy grail of homeownership, become worthless eight years ago when low rates and falling prices so reduced the value of the interest that owners can deduct that the MID has minimal impact?

Even when the MID is combined with the dedication owners receive for property taxes, would many middle class homeowners do just as well tax-wise by renting?

“We believe we have found one of the primary reasons why entry-level home buying has not recovered—and why homeownership has been plunging,” wrote real estate consultant John Burns in an eye-opening blog post circulated April 13, two days before income tax deadline day.

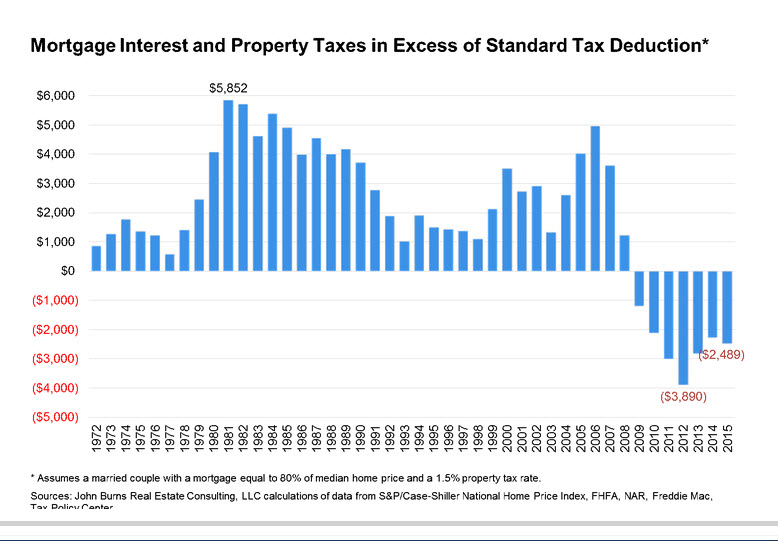

The standard marital deduction has risen from $1,300 in 1972 to $12,600 today, meaning that the first $12,600 of itemized deductions has no benefit to consumers. Today, a typical first-time home buyer financing 95% or less of a median-priced US home pays less than $12,000 in mortgage interest and property taxes, which is not enough to warrant itemizing. Even with other deductions that bring the taxpayer over the $12,600 limit, the tax savings are minimal, argues Burns.

“In the graph below, we show the change over time for a typical homeowner couple with an 80% loan-to-value mortgage and a 1.5% property tax rate on the median-priced US home. That owner paid mortgage interest and property taxes in excess of the standard deduction every year from 1972 to 2008. Today, that homeowner’s deductions fall nearly $2,500 short of the standard deduction,” Burns wrote.