Next September, two months before the Presidential election, America celebrates eight years since the Treasury Department took over Fannie Mae and Freddie Mac and turned them into wholly owned subsidiaries. Since then the federal government’s control over the nation’s housing markets has grown even greater than ever.

While we’ve been waiting for policymakers to fix a broken system of housing, the GSE’s and government programs like FHA are using taxpayer-backed credit to make the housing recovery possible—first to keep virtually all credit flowing in the crisis years, now to open the door to homeownership to more marginal borrowers.

If you’re a first-time buyer or have a less than golden credit past, you’d be crazy to go anywhere else than the government for a mortgage—either a GSE low down payment conforming loan program or a direct federal program like FHA. Not only do you stand a much better chance of qualifying., even the premium payment on FHA mortgage insurance has been lowered to make the decision easier.

The latest Urban Institute credit availability index (HCAI) shows that although both private and public mortgage credit availability remains above the record low of 4.6 in the third quarter of 2013 (Q3 2013), it has trended downward over the past four quarters. The HCAI measures the percentage of home purchase loans that are likely to default—that is, go unpaid for more than 90 days past their due date. A lower HCAI indicates that lenders are unwilling to tolerate defaults and are imposing tighter lending standards, making it harder to get a loan. A higher HCAI indicates that lenders are willing to tolerate defaults and are taking more risks, making it easier to get a loan.

However, mortgage credit availability in the government-sponsored enterprises (GSE) channel—Fannie Mae and Freddie Mac—has been at the highest level over the past three quarters since the low hit in 2010. Credit availability in the government channel (FVR), which comprises the Federal Housing Administration, the Department of Veterans Affairs, and the Department of Agriculture Rural Development program, has decreased over the past four quarters, although it is still above its record low in 2013.

The GSE market has expanded the credit box for borrowers more effectively than the government channel has in recent months. The downward trend of credit availability in the GSE channel was reversed in Q2 2011. From Q2 2011 to Q3 2015, the total risk taken by the GSE channel increased 50 percent, from 1.4 percent to 2.1 percent.

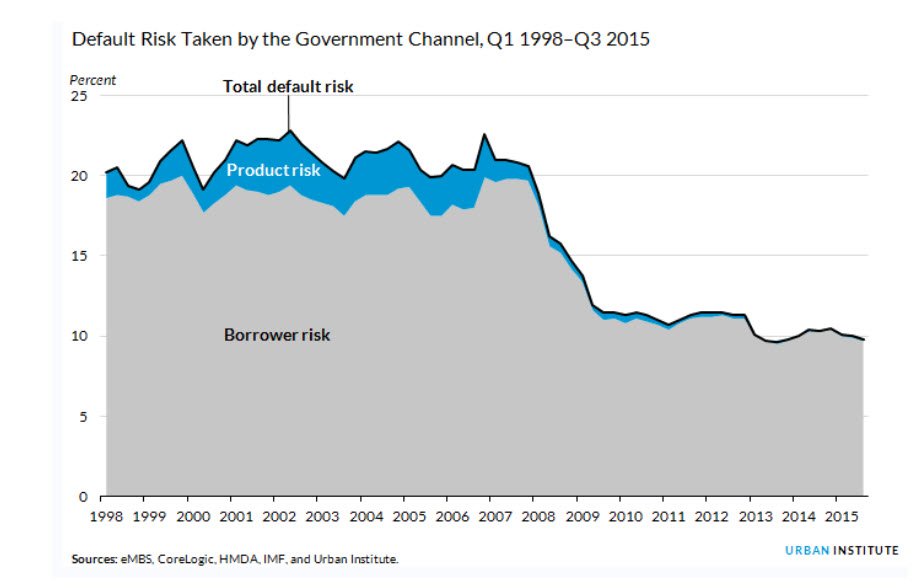

The total default risk the government loan channel is willing to take bottomed out at 9.6 percent in Q3 2013. It climbed to 10.5 percent in Q4 2014 but has dropped slightly since then and stood at 9.8 percent in Q3 2015. The 9.8 percent credit risk for the government channel is just under half the pre-bubble level.

By contrast. credit availability in the portfolio and private-label securities channel continued to stay below the record-low 3 percent established in 2013. The portfolio and private-label securities channel took much higher product risk than the FVR and GSE channels during the bubble. After the crisis, the channel’s product and borrower risks both dropped sharply. They have stabilized since 2013, with product risk fluctuating around 0.6 percent and borrower risk around 2.0 percent between 2013 and 2014. The total default risk taken by this market is currently at 2.4 percent, which matches its record low.

Here’s another way to look at the differences between private and public sector lending. The latest date from Ellie Mae confirms the wisdom of going government if you’re a first-time buyer looking for a mortgage. At 651. median FICOS for FHA purchase loans closing in December were 105 points higher than purchase conventional loans, at 754, an immense gap. If you are carrying a debt load the gap is also huge. Median front end dent to income ratios in December were 28 for FHA purchase loans compared to 23 for conventional. The difference between media closed loan to value ratios was also huge—a 97 median for FHA, 81 for conventional.

Despite the federal help, the first-time buyer share in 2015 disappointed those who thought it would the “Year of the First-time Buyer,” dropping below 20 percent in February and ending the year at 32 percent in December, far below the 40 percent once considered typical.